May 2026 Market Commentary

Market Update and Economic Developments

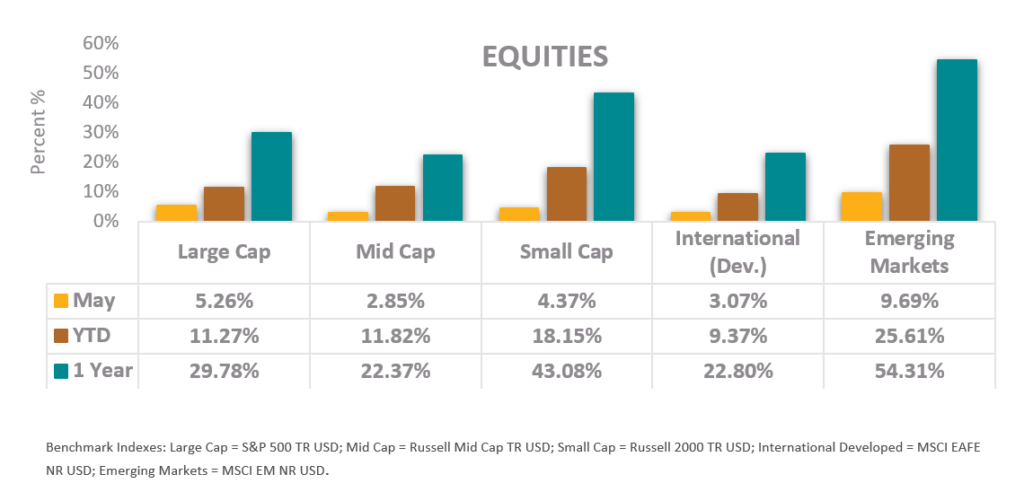

- The S&P 500 posted a strong 5.26% return in May, finishing the month at record highs and bringing the year-to-date return to 11.27%. This marks a strong reversal from the market low at the end of March, with the index rallying close to 20% since the market bottom. Technology led the advance with strong earnings, as Nvidia rallied following its quarterly earnings report and the launch of a new processor, reinforcing the artificial intelligence theme that continues to drive much of the market’s leadership.

- Emerging Markets were the standout performer, returning 9.69% in May and extending a run that brings the one-year return to over 50%. Small Cap stocks gained 4.37%, bringing their year-to-date return to 18.15%, while Mid Cap and International Developed stocks advanced 2.85% and 3.07%, respectively. The breadth of the rally beyond U.S. large cap names was a welcome development, especially as equity markets outside of the United States rebounded from geopolitical developments in the Middle East with positive performance.

- US GDP growth was modest to start the year. The Bureau of Economic Analysis’s second estimate, released in late May, showed real GDP expanding at an annualized rate of 1.6% in the first quarter, an improvement over the 0.5% pace in the fourth quarter of 2025, which had been depressed by the federal government shutdown. Business investment in equipment was a notable contributor, driven in part by continued spending on artificial intelligence infrastructure, while consumer spending decelerated. Inflation readings came in higher than last month due to the rise in energy prices. The risk of prolonged high energy prices lies in increased inflation down the supply chain for goods and services.

Fixed Income Market Update

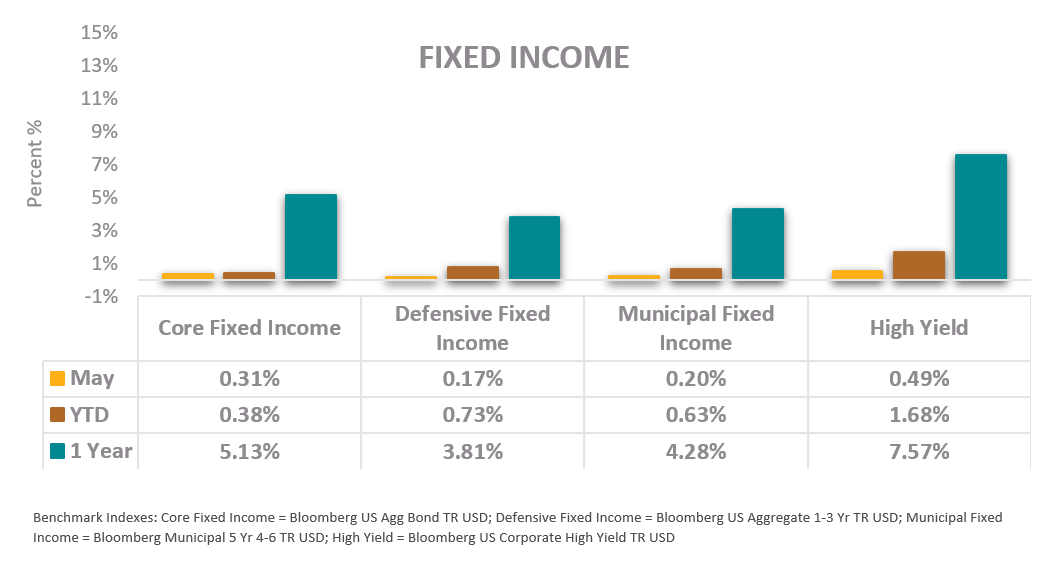

- The yield on the 10-year Treasury rose over the course of May, ending the month near 4.45%. Core fixed income, as measured by the Bloomberg US Aggregate Bond Index, posted a modest gain of 0.31% for the month. Across fixed income sectors (short duration, municipal, core and high yield), returns were generally positive but muted, with High Yield leading at 0.49%.

- The Federal Open Market Committee did not hold a meeting in May; at its late-April meeting, the Committee left the federal funds target range unchanged at 3.50%–3.75%. Notably, the decision drew four dissents, an unusually high number reflecting a widening divide on the Committee. FOMC meeting minutes released during May indicated that some members viewed further rate increases as possible should the conflict in the Middle East continue to aggravate inflation. Futures markets are pricing in a high probability of no change at the June meeting, and a moderate chance by year-end for rate hikes. Many are speculating how Kevin Warsh, who began his term as the Chair of the Federal Reserve in May, will lead the Fed following predecessor Jerome Powell. Warsh so far has advocated publicly for balance sheet reduction and less intervention in markets from the Fed.

Mission’s market and investment commentaries reflect the analysis, interpretation, and economic views and opinions of our investment team. They are not intended to provide investment advice for any individual situation. Please contact us if we can provide insight and advice for your specific needs.