April 2026 Market Commentary

Market Update and Economic Developments

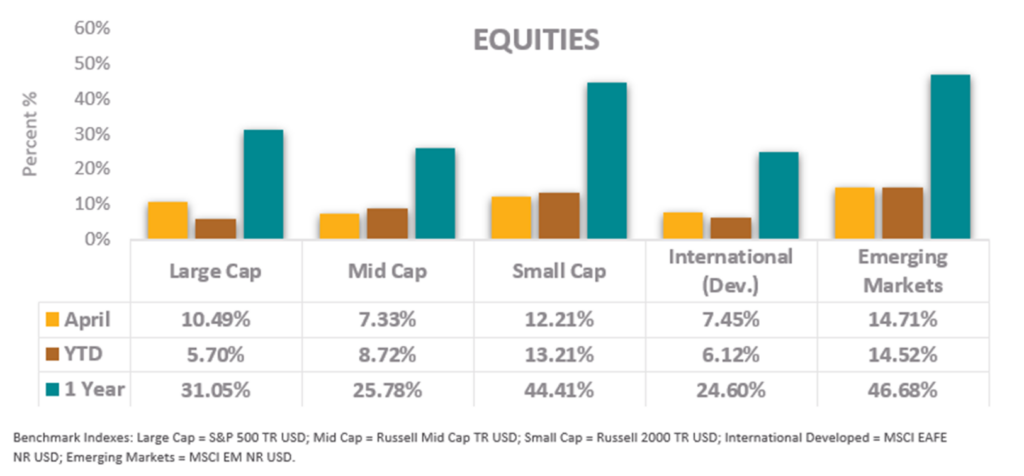

- April saw a sharp rebound in equities following March’s geopolitics-driven selloff, as easing concerns around energy supply disruptions and strong corporate earnings growth lifted markets broadly. With earnings season in full swing, year-over-year Q1 earnings growth is on pace to increase by approximately 27%. Large cap equities led the recovery with the S&P 500 gaining 10.49%, driven primarily by strength in energy, materials, and industrials, as mega-cap growth stocks rebounded, and AI-related names regained momentum. Cyclical leadership also emerged, with Industrials and Consumer Discretionary benefiting from improved risk appetite. Small caps outperformed at 12.21%, reflecting greater sensitivity to easing financial conditions, while mid-caps rose 7.33%. Developed international markets advanced 7.45%, supported by gains in exporters and industrials, and emerging markets posted the strongest gain at 14.71%.

- Emerging markets equities have led in 2026, returning 14.52% year-to-date, supported by strong earnings growth, AI investment in tech-driven markets like Taiwan and South Korea, and a weaker U.S. dollar. With emerging economies projected to grow roughly 4%+ in 2026 according to Merrill, performance continues to outpace developed markets and enhance the asset class’s appeal.

- Mission Trust portfolios grow by investing in a mix of U.S. and international stocks, so you benefit from opportunities around the world. We regularly adjust where we invest based on where we see the best potential and combine that with a thoughtful mix of investments to help manage ups and downs—keeping your portfolio moving toward your long-term goals.

Fixed Income Market Update

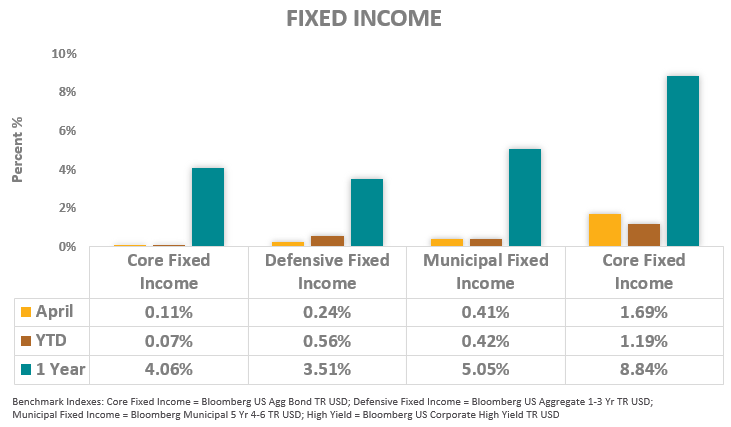

- Fixed income provided modest stability in April, with most sectors delivering positive but subdued returns amid a strong equity rally. Core fixed income gained 0.11%, Defensive fixed income rose 0.24%, and municipal bonds added 0.41%, while high yield outperformed at 1.69%, benefiting from improved risk sentiment. Year-to-date, returns remain muted across the traditional fixed income sectors as core and municipals face continued headwinds due to elevated interest rates.

- Recent comments from Federal Reserve Governor, Christopher Waller, point to a subtle shift in how policymakers view the labor market. Rather than signaling renewed weakness, the Fed appears more comfortable holding rates steady due to structural constraints on labor supply. Slower immigration and an aging population kept labor force growth near zero in 2025, lowering the pace of job creation needed to sustain stable unemployment. As a result, volatile monthly payroll prints may reflect a new equilibrium rather than deterioration, though softer hiring trends still warrant caution and support a near-term pause in policy. The Bureau of Labor Statistics’ estimates suggest that labor force growth could be flat in 2026 because the economy doesn’t need to add as many jobs as before to keep the unemployment rate steady.

Mission’s market and investment commentaries reflect the analysis, interpretation, and economic views and opinions of our investment team. They are not intended to provide investment advice for any individual situation. Please contact us if we can provide insight and advice for your specific needs.