March 2026 Market Commentary

Market Update and Economic Developments

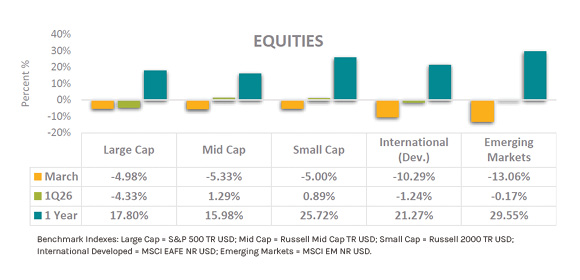

- March saw a relatively dramatic pullback in equities across geographies, with the S&P 500 recording nearly a 5% loss for the month and international stocks down more than double domestic stocks. Much of this stress on the market can be attributed to the war in Iran and the closure of the Strait of Hormuz, which has put upward pressure on energy prices throughout the world. Although March performance was poor across geographies and company sizes, year-to-date (YTD) performance is more varied. The Magnificent Seven megacap stocks are responsible for 83% of the S&P 500’s YTD return of -4.33%, with all seven companies underperforming the index. Smaller companies faired much better, with Mid-Cap stocks at a 1.29% YTD return and Small Caps not far behind at 0.89%. Emerging Markets had a very strong start to the year and ended March nearly flat for the quarter despite a drop of more than 13% during the month.

- Some of the weakness in performance from megacap tech stocks could be attributed to a broader decline in sentiment in software stocks. Media attention, particularly in the first part of the quarter, highlighted a future in which artificial intelligence may render many software companies obsolete. In the first quarter, the S&P North American Technology Software Index was down over 24%. Some analysts point to increased productivity gains—ostensibly from the use of artificial intelligence—as proof that AI will replace workers and companies over time, especially in the software industry. However, it is important to note that some productivity gains may be the result of a declining labor force due to decreased immigration. Since productivity is essentially measured by dividing output by labor, productivity can grow both through increased output, decreased labor, or a combination of both.

- Although a 4.33% drawdown in the S&P 500 is uncomfortable for investors, it is not out of the ordinary. Since 1980, the S&P 500 has experienced an average maximum intra-year decline of over 14%, despite having a positive calendar year return in 35 of 46 years. Investors who stay invested and diversified despite the volatility have been rewarded time and time again for their discipline and patience over the long term.

Fixed Income Market Update & Other Assets

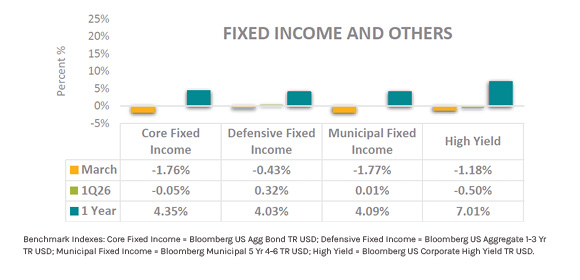

- Fixed income provided some ballast relative to falling equities, declining 1.76% in March due to rising longer term interest rates and ending the first quarter of 2026 nearly flat. In years past, a low correlation between stocks and bonds was helpful during periods of equity volatility; for example, when equities were negative in 2001, 2002, 2008, and 2011, bonds were positive. However, periods of high inflation present a major headwind to both stocks and bonds. More recent equity declines in 2022 and the first three months of 2026 have resulted in negative returns for both asset classes.

- At it’s March meeting, the Federal Reserve elected to maintain the benchmark interest rate of 3.50% to 3.75%. In addition to geopolitical uncertainty in the Middle East, Chair Jerome Powell reiterated in his press conference that although job gains are low, inflation has remained well above the Fed’s 2% target. Mr. Powell acknowledged that there is some merit to the idea of “looking through” exogenous energy shocks that spike inflation in the short term, but he emphasized that elevated inflation over the past five years warrants caution and patience.

- Although gasoline prices have risen substantially due to the closure of the Strait of Hormuz, retail gasoline prices of nearly $4 per gallon as of 3/31/26 are still far below 2022’s high of over $5 per gallon. Should oil prices continue to climb, the U.S. economy is much more resilient to oil shocks than it has been in the past. Prior to 2008, net imports of petroleum and related products had reached 3% of the U.S. nominal GDP. Since then, the U.S. has steadily decreased its dependency on international oil and is now a net exporter rather than a net importer, which should help to insulate the U.S. from the effects of higher oil prices.

Mission’s market and investment commentaries reflect the analysis, interpretation, and economic views and opinions of our investment team. They are not intended to provide investment advice for any individual situation. Please contact us if we can provide insight and advice for your specific needs.